How Much Home To Buy?: Lesson Four

Closing Costs, Levering Up

Welcome back to the Theopetra Testament. Subscribe now so you don’t miss our weekly educational posts bridging the gap between cryptocurrency and real estate. This post, composed by our Self-Repaying Home team, will give you a brief update of financial markets in relation to housing before diving into the fourth part of our series on getting ready to purchase a home.

Market Update:

Current Mortgage Rate: 4.27%, another new 12-month high (Bankrate.com)

Markets continue to take their cue from geopolitical headlines, and with market participants getting more comfortable with the uptick of war headlines, focus has begun to shift back to global inflation. This week’s CPI report showed inflation at 40 year highs and increasing at a 7.9% pace – at the same time Jerome Powell spoke to Congress and effectively gave the green light for a 25 basis point hike this month.

Somehow even with inflation climbing at a torrid pace over the last 6 months (last 6 CPI prints: 5.4, 6.2, 6.8, 7.0, 7.5, 7.9), it took until this week for the Fed to officially wind down and end its QE asset purchase program; this week saw the final Fed liquidity injection into markets.

With front end rates backing up to price in ~7 hikes over the next 12 months and 2 year yields hitting new highs (~1.75%), the yield curve made new flats and officially inverted with 10 year yields now lower than 7 year yields. This signals the market is beginning to price in a policy error, as investors look to put cash to work further out the yield curve to ‘ride out the coming storm.’ Of course, not helping pending recession talk is oil, which is now over $100/barrel and has a perfect track record of predicting recessions (every time oil has hit $100/barrel, a recession has followed).

With this said, risk markets remain volatile with S&P 500 now sitting at ~12% off the highs, while the Nasdaq is officially in a bear market and 20% off the highs. So putting it all together, stocks are in a bear market while rates are at 0, inflation is at 40 year highs, and the Fed is expected to hike 7 times in a market wrought with supply chain issues it has no control over.

Lol.

Interesting Housing Headlines

“Phoenix’s ‘Tent City’ expands to nearly 1,000 as housing affordability crisis worsens [...] the camp more than doubling in size in two years a testament to how bad the Phoenix housing crisis has become” (Vice)

“Millennials [who makeup 37% of all home buyers nationally] are bypassing the traditional starter home for their dream home” (Yahoo! Finance)

Lesson Four: Entering The Trade

So you’ve now come to terms on the realization you are going to complete the biggest transaction of your life and buy a home. Congrats! Let’s first take a step back and think about how you will now no longer be ‘short’ the real estate market, but instead ‘flat’:

If you own 0 real estate ... you are unfortunately ‘short’ the housing market. The only way this works is if housing prices drop, and thus you are short the asset (house) price. Any rise in home prices makes a future purchase that much more costly, particularly given the inherent levered nature of real estate. For example, if home prices rise a ‘modest’ 4% annually, over a 5 year period the ‘average’ home price grows from $400K to ~$488K, and the down payment required grows from $80K to ~$98K – a 22% increase in down payment!

The cost of not being in the market is exponentially more than one may think.

If you own 1 house ... you are ‘flat’ the housing market. Your ownership stake effectively protects you from any future rise in home prices should you want to move to a new house down the road. And by owning one house, you’ve officially caught the HPA (Home Price Appreciation) wave; do everything you can to stay on it.

The HPA wave will be your lifeline in a bull market, and a key to preserving wealth.

If you own 2 or more houses ... you are officially ‘long’ the housing market. This is due to the fact you can sell 1 house (if prices rise and go parabolic, like in today’s market) and not have to automatically reinvest the proceeds to stay on the HPA wave. Rather than be simply on the wave, you are now ‘in the trade.’

A material move higher in real estate will grow your wealth, rather than preserve your wealth.

How Much Of The Trade To Put On

This answer to ‘what can I afford’ is going to vary significantly from person to person. With that said, there are a couple consistent starting points:

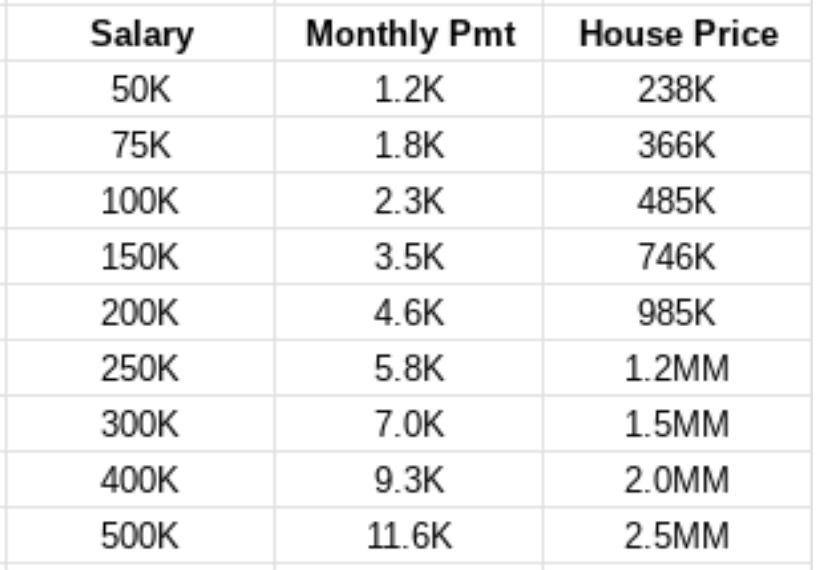

- Most ‘financial advisors’ recommend spending no more than 28% of your gross income towards your mortgage. Working with round numbers, this means if you make $100K/year, your annual mortgage payment should be no more than 28K, or $2,300/month. This monthly payment works to a $485K home price.

- Historically, the average home price is ~5x household income. This actually checks out in the above example, where a solo earner making $100K who wants to purchase a house with ‘responsible’ leverage would be buying a house at 4.85x earnings.

We’ve put together a quick table showing 1) salary, 2) 28% rule, and 3) corresponding house price that one could ‘afford’:

Unfortunately, given the ripper the housing market has been on since the pandemic and raging asset price inflation, home prices as a multiple to household income have now surpassed 2008 housing bubble levels (LongTermTrends) and are at an all time high:

This means that, in theory, either housing prices have to cool off or wage growth has to materially pick up for this multiple to ‘get back in line to historical averages.’ With home prices at ~7x household income, this means the same 100K earner is effectively having to pay 700K for a house that historically (literally anytime before 2020) would have cost $500K.

Buying in this market then forces the borrower to incur a $3,300/month payment, up $1K a month! Suddenly, the mortgage payment is now eating up nearly 40% of an earner’s income, a big red flag and ‘no no’ in the underwriting world.

Ride that HPA wave. Otherwise, you’re stuck with either too much leverage impacting your spending in other places (vacations, savings, food, etc) or a ‘quality of life’ downgrade where the quality of your shelter is behind your peers (ie, in the above example, you are forced to level down to a $500K home).

Go Big or Go Home?

By now the only question regarding the HPA wave is if you are going to start out surfing on the east coast (starter home) or go right to Pipeline and the North Shore (‘dream home’). Historically, the popular trade for first time home buyers has been to begin with a starter home.

With that said, this trend is changing for a few reasons: 1) most starter homes in desirable neighborhoods have been torn down and rebuilt into mansions for those who are already on the HPA wave, reducing ‘affordable’ supply, 2) the younger generation who would make up majority of first time home buyers - successful millennials - have a larger than historical average savings amount for down payment (due to several factors including recent market performance, starting home buying process later in life, etc) and 3) savvy borrowers are beginning to realize how cumbersome and expensive each real estate transaction can be.

Zeroing in on the last part a bit more, closing costs can be thought of as the cost of transacting in real estate. These fees are unavoidable and vary between 2% and 5% of the borrowed

amount. For example, a $400K property with 20% down has a loan amount of $320K and thus, the closing costs are between $6.4K and $16K.

This is effectively a hidden tax and penalizes individuals who are moving at a frequent pace. This is important to note given any starter home that is then flipped to ‘level up’ to the dream home will incur this cost; this cost is substantial given it eats away into one’s profits when riding the HPA wave.

At Theopetra we are looking at rethinking the home buying process and will use our innovative structure to dramatically reduce these closing costs.

The Inflation Kicker: 4% =! 4%

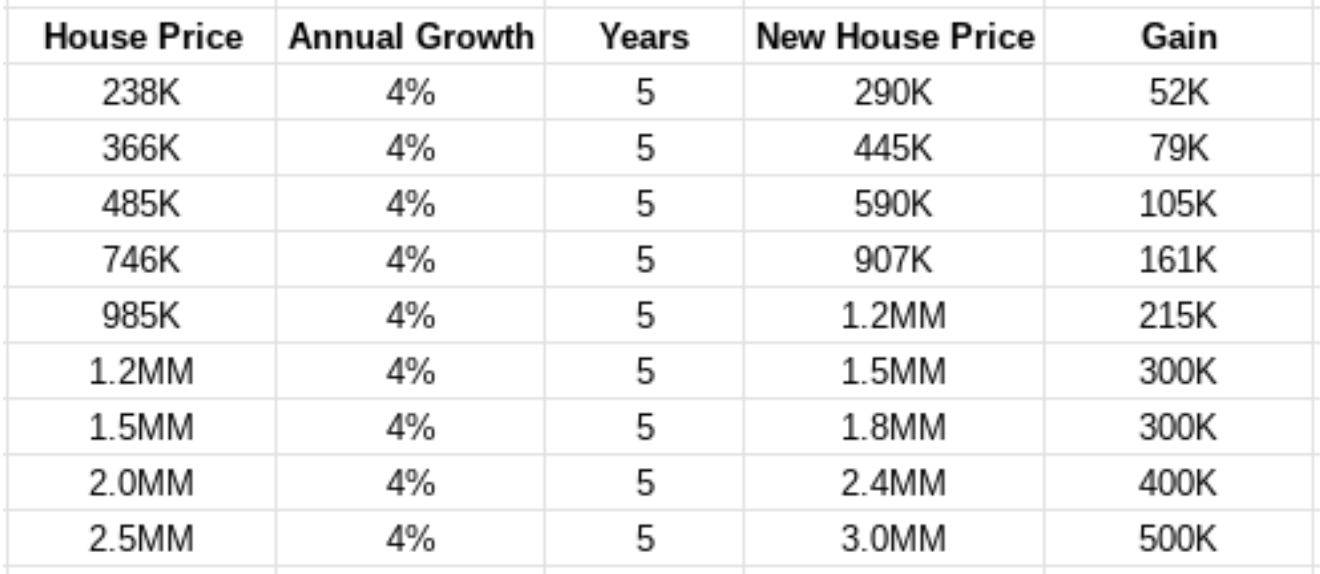

As home prices appreciate the inherent nature of leverage makes affording a ‘dream home’ harder and harder. As we noted earlier, annualized 4% growth over 5 years turns the ‘average’ home price from $400K to $480K. But look at what it does to the ‘dream property’ that’s $800K – it grows into a $973K property, a $173K increase in price!

Below is a table that breaks down this HPA growth by house price, as organized from home prices in table 1:

As illustrated above, the sooner and earlier you can afford a ‘dream home,’ the faster you should level up and ‘bite the bullet’ when levering up to buy a house. The outright pace of home price appreciation makes the $ value that much more difficult to obtain and costly when looking at more expensive homes. And remember, the closing costs (ie transaction costs) will also eat into your ‘starter home’ profits.

For many, it may make sense to stretch the budget in a responsible manner and grow into the home rather than settle for a starter home to later flip.

Wrapping It Up and Next Steps

In this fourth installment, we’ve gone in depth on the impacts of leverage and home prices, illustrating simple to understand examples that show the power of home price appreciation and leverage. Remember, home owners have all the leverage and the ‘return’ on a rent payment is always 0%.